There is a common perception in the investment world that active managers have an advantage over passive managers during times of increased volatility, since active managers can go on the defensive, whereas passive managers have strict mandates to mimic an index.

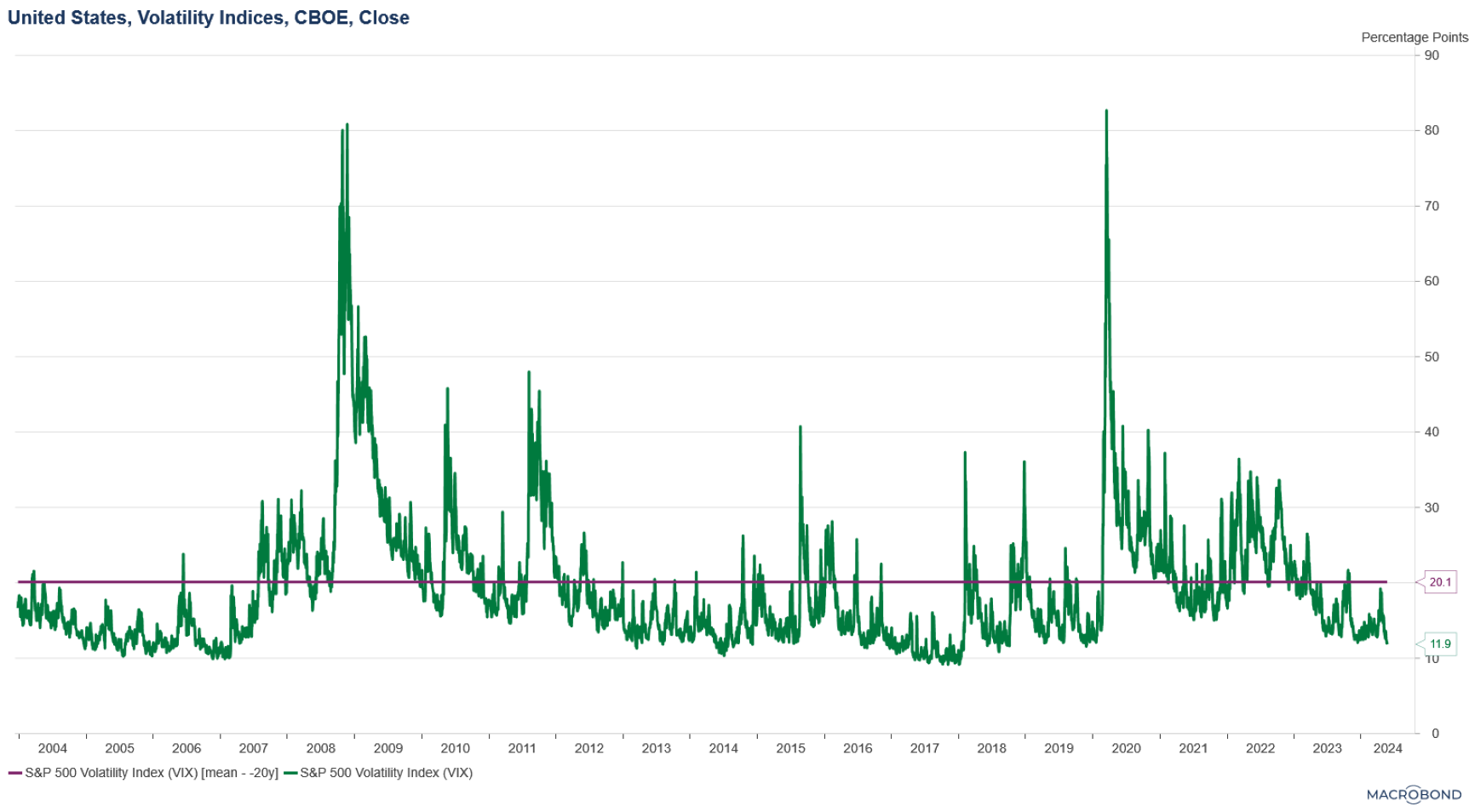

After an extended time period (2012 – 2019) where equity volatility, measured by the CBOE VIX index, traded below its 20-year average of 20.1, volatility increased during the peak of the pandemic. After a bout of low volatility in 2021, volatility surged above its 20-year average in 2022. However, equity volatility fell below its 20-year average and remained there throughout the first quarter (figure 1).

Click to enlarge

Despite the ongoing uncertainties about monetary policies and the pace of monetary easing, the S&P 500 index posted a +10.56% return during the quarter, which corresponds to the fall in volatility. With the lower volatility and strong equity market performance, let’s take a look at how actively managed separately managed accounts fared against their passively managed counterparts during the quarter.

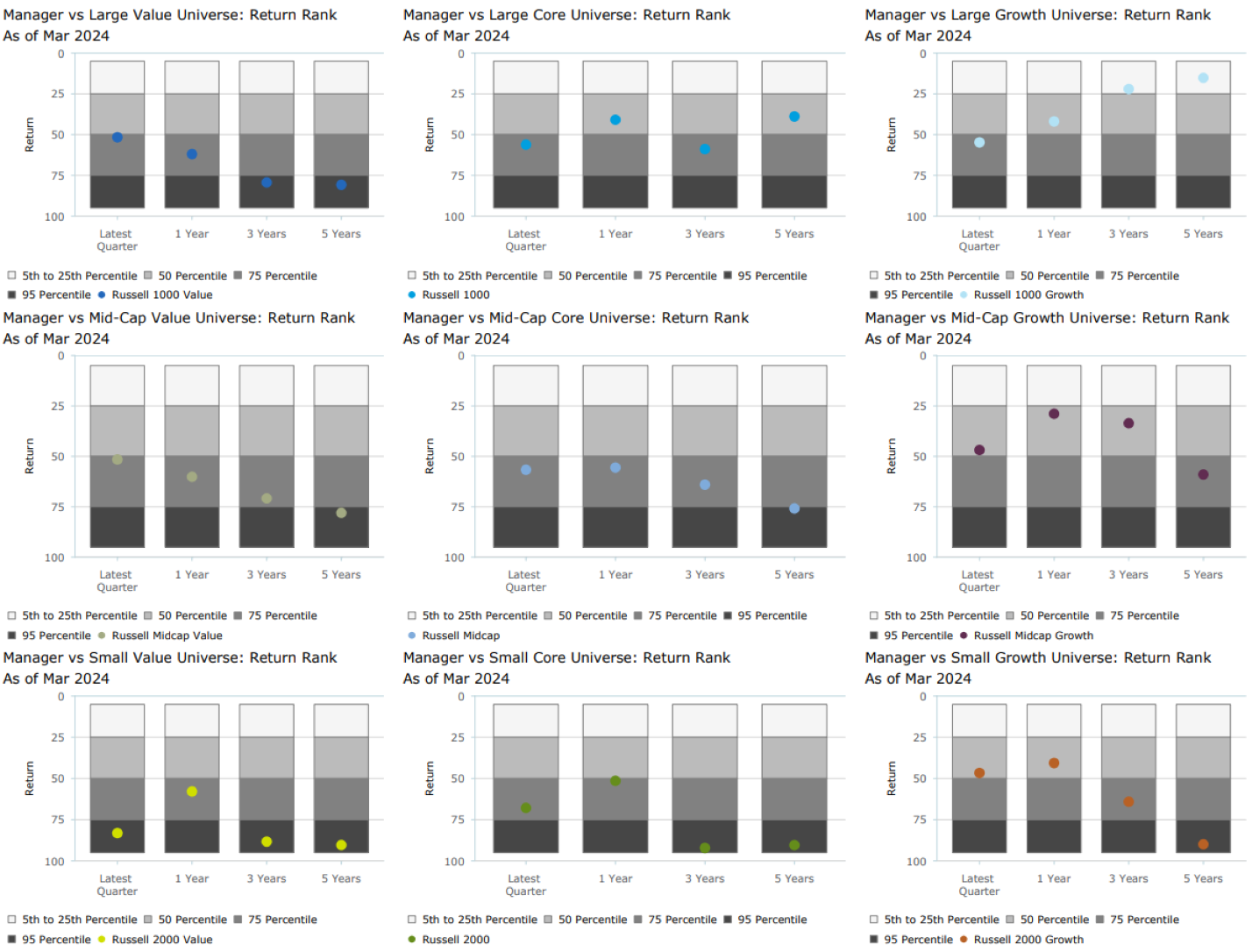

As you can see in the graph below, U.S. actively managed equity SMAs fared well during the quarter. The mid-cap growth and small-cap growth styles were the only equity styles that saw an advantage for passive SMAs, albeit a small advantage, with just under 50% of the active managers beating their respective benchmarks.

As for the large-cap space, which tends to be a more efficient investment style, making it harder to find consistently outperforming active managers. During the first quarter, large-cap actively managed SMAs held their own, as about half of all active SMAs beat the respective style benchmark across all three styles. Large core and large growth managers fared the best with slightly more than 50% of active managers beating the benchmark.

As many may expect, the biggest winners came from the small-cap styles. Over 75% of active small-cap value SMAs beat the Russell 2000 Value index, which wasn’t an extremely tough hurdle as the index posted a +2.9% return. Meanwhile, roughly 70% of active small-cap core SMAs beat the Russell 2000 index, which was a slightly tougher hurdle as the index posted a +5.18% return.

Click to enlarge

The pace of market moves has increased over the years, which makes it important to strive to create diversified asset allocation strategies that can withstand the different financial market dynamics and changing investment landscape. It’s also important to note that research shows there are some equity styles that tend to benefit active management over passive management. When building an investment portfolio, it’s prudent to take an inclusive view rather than an exclusive view of the active versus passive debate.

Ryan Nauman is the Market Strategist at Zephyr, an Informa company